The global tanker market has been weak (again) since mid-2020. The spectacular recovery seen in containers, LNG and dry bulk throughout 2021 has not yet extended itself to tankers. Truth be told, most market participants were expecting this to happen for most of the year, but here we are already in November.

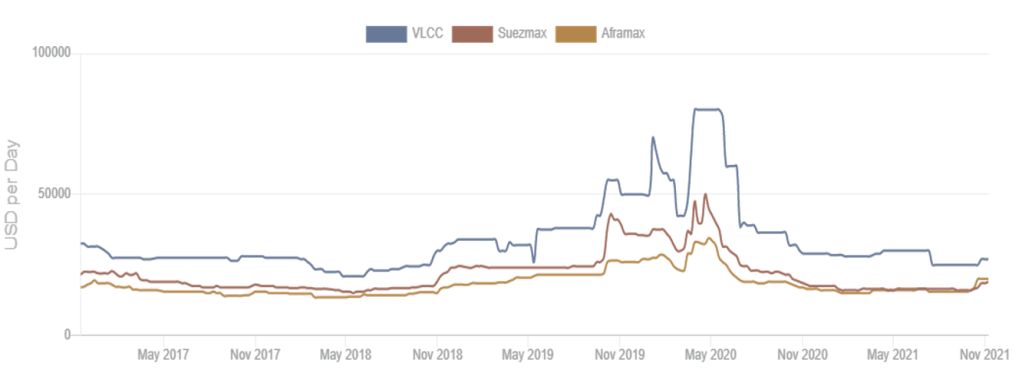

According to Fearnleys data, average dirty 1-year T/C rates currently stand at $27,000 per day for VLCCs, $19,000 for Suezmaxes and $20,000 for Aframaxes.

This means international tanker operators are still bleeding, with most of the listed carriers reporting deficits for 3Q 2021.

The three main Latin American operators, however, are not as exposed to short-term market developments. Venezuela’s PDV Marina lies in ruins after years of poor management and US-led sanctions. But the other larger two state-owned tanker companies, Ecuador’s Flopec and Brazil’s Transpetro, are in better shape. Their oil conglomerate sponsors, respectively Petroecuador and Petrobras, not only provide long-term contracts for their shipping subsidiaries, but also are the absolute dominant force in their own national production.

Flopec, however, is being held back by contracts of chartered-in vessels at high rates in 2020 and Transpetro is still struggling to make the overpriced Promef fleet profitable.

Meanwhile, their loss-making international competitors are patiently waiting for the market to turn. And even if it does not happen tomorrow, the long-term prospects for tankers in South America looks rather bright, especially for the shuttle tanker and conventional crude segments.

Shuttle tankers are a niche business, heavily concentrated in two main areas: The North Sea and the Brazilian east coast. Fearnleys data puts the current fleet at 77 vessels, with 85% of them controlled by just three groups: market leaders KNOT/KNOP and Altera (formerly Teekay Offshore Partners) tied at the top, with Singapore-based AET following with the largest orderbook.

Rystad Energy data points out that future growth in offshore oil production, and therefore demand for shuttle tankers, will mainly come from Brazil. North Sea oil production shuttle tanker volumes are expected to grow by 27% over the next decade, while in Brazil that figure would be 63%. Another relevant growth market is the Guyana-Suriname basin, the darling of oil markets for the last few years.

ExxonMobil has reached the staggering figure of 10 billion barrels of oil equivalent (boe) discovered offshore Guyana, or about 11.5% of global cumulative conventional discovered volumes between 2015 and 2021.

Moreover, KNOT Offshore Partners (KNOP) stressed during its Investor Day in early October that “shuttle tanker charters are typically a very small component of our customers’ field operating costs”, and that “shuttle tankers service is a growing proportion of all offshore production, recently surpassing 90% in Brazil”.

Due to their mostly long-term contracts with top oil majors, shuttle tankers’ finances are more stable and currently way healthier than conventional tankers. KNOP, for example, remains profitable and has distributed cash to shareholders for 25 quarters in a row. Still, in Q2 2021, the company was pushed to a one-off deficit due to a big write-down to one of its vessels, the Windsor Knutsen.

The expected surge in oil production offshore Guyana-Suriname and Brazil will not only keep shuttle tankers busy, but also their conventional Suezmax and Aframax cousins. Even VLCCs are likely to be affected, as a few VLCC cargoes have already been dispatched from Guyana. Brazil is increasing the employment of larger vessels for lifting exports, especially the loadings at Porto do Açu.

According to the National Agency for Petroleum, Natural Gas and Biofuels (ANP), Brazil is currently exporting 1.4m barrels per day (bpd) by sea, a figure that is expected to surpass 2m bpd within this decade. In Guyana, Exxon is forecasting production at 800k bpd by 2025 and 1m bpd by 2027, against 120k currently.

Elsewhere in South America, companies are dusting off expansion plans after the oil price upsurge. Reuters reported Ecuador’s plans to attract $14 billion to double its oil production from 500k bpd to 1m bpd.

Colombia and Argentina have expansion plans as well, but the latter is particularly bullish on production increases due to the Vaca Muerta (Dead Cow) shale play.

Gibson Shipbrokers agrees. On its Week 43 report, the London-based house argued that “any increase in crude exports loading out of Argentina would be positive for Suezmax and Aframax tankers and provide additional support for the Atlantic tanker market”.

However, it remains to be seen if volume growth will result in better earnings for operators. For now, this could be the case, as owners are holding back their ordering impulses. In a previous report (Week 36), Gibson pointed out that the “orderbook remains restricted, despite fresh orders and limited scrapping activity. The Aframax/LR2 and VLCC orderbook stands at just over 10% of its existing fleet, the Suezmax orderbook is at 9.2%”.

The crude tanker market in South America is thus one of tough times, but high hopes.

__________________

Subscribe to our Weekly Newsletter and get the best of Latin America’s maritime business. It’s free!